I offer this newsletter to provide insight into current information and trends in business and the appraisal industry. I hope you find it enriching and welcome any questions or comments you may have. If there is a topic you'd like me to discuss or report upon let me know.

We provide services including business valuation, divorce consulting, litigation support, forensic accounting, transaction due diligence, and operations consulting. For further information about our practice please visit GRWAppraisalServices.com. You may email me at GRWAppraisal@Gmail.com or call me directly at 512-574-3444 Enjoy! Greg Weichbrodt - Principal

This writing presents a discussion of the value of voting rights and a primer on buy-sell agreements.

The Value of Voting Rights

Many companies maintain two or more classes of stock. When valuing different classes of stock in a company one must identify the differences in rights and privileges between the classes. Oftentimes only a single difference exists, wherein one class of stock enjoys the right to decide and vote on corporate issues and another class does not. In such an instance it is necessary to determine whether this right affords a voting shareholder greater economic benefit than a nonvoting shareholder. To do so an appraiser may first turn to documents such as shareholder agreements, articles of incorporation, or corporate bylaws to determine whether there is a formal agreement in place among shareholders pertaining to voting rights and privileges. At times these documents do not explicitly or clearly articulate items subject to vote nor necessary percentages interest required for approval of certain actions. Consequently, some provisions may be subject to state statutes.

A voting shareholder could presumably vote on key shareholder provisions such as distributions, electing directors, amendments to corporate documents, stock transfers, or the potential sale or liquidation of a company. Therefore, voting shareholders virtually always have the ability to derive greater economic benefit than nonvoting shareholders.

Empirical Evidence

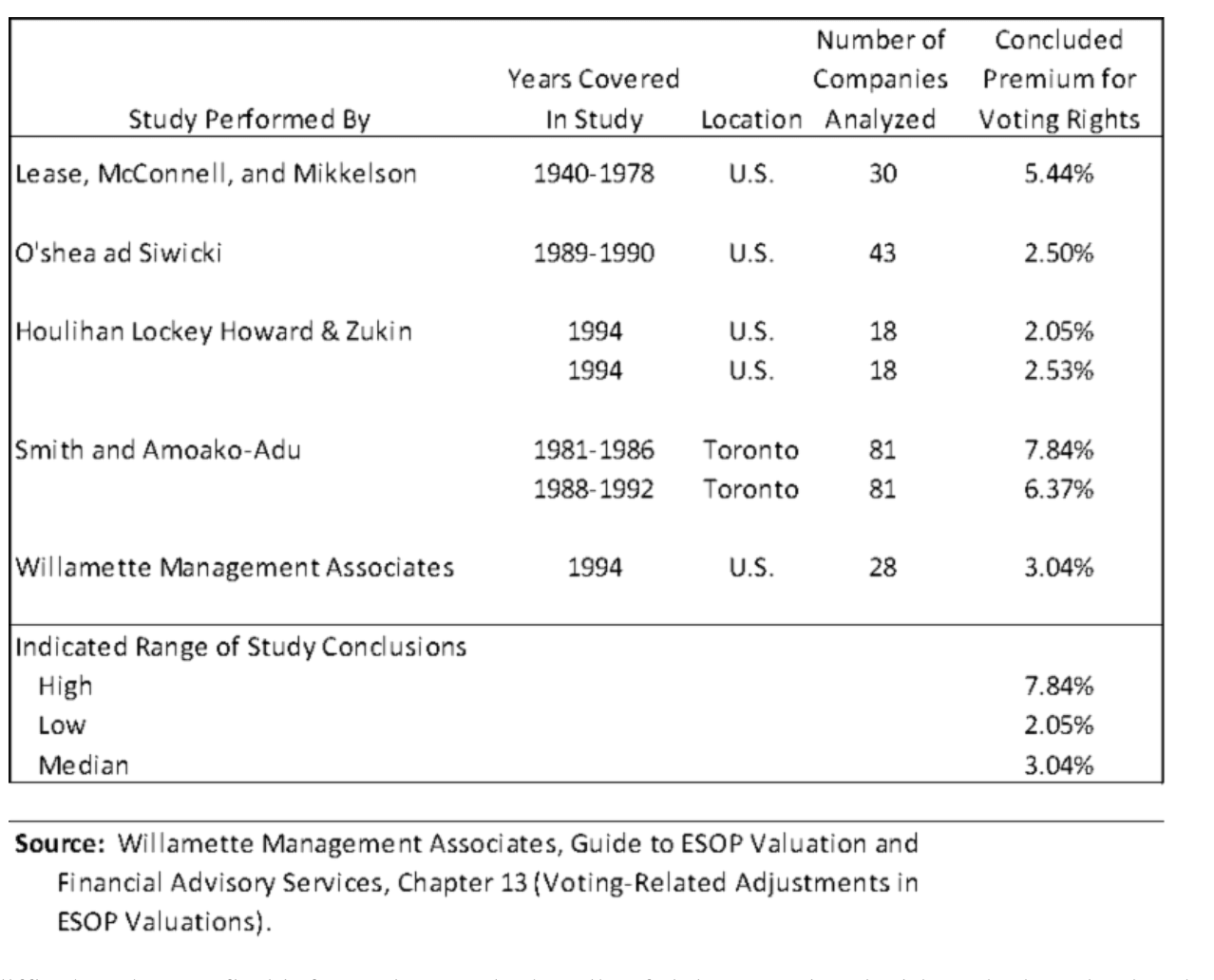

After the differences in rights between voting and nonvoting shares have been identified, the critical issue is to estimate the impact on share value. There have been a handful of major published studies of publicly traded companies with more than one class of stock. These studies attempt to isolate instances in the public markets where two or more classes of stock were traded on the open market with identical rights and privileges except for where one class had the right to vote and the other did not. The following table provides a summary of the most notable of these studies.

It is difficult at best to find information on the bundle of rights associated with each share in the above studies. So, it is difficult to comparatively assess whether the voting rights associated with your subject shares are more or less valuable than the indications provided in the empirical studies. By looking at statutory differences in class rights, we can estimate whether a company's stated class rights are comparatively similar, superior, or inferior to those generally delineated by statute. We use this information and an approximate value range from studies like those above to make an informed judgement on the value of a company's voting rights. Keep in mind that corporate governing documents and court precedent may dictate whether different share classes are to be treated differently.

See Estate of Simplot, 112 T.C. 130, 173 (1999) and Estate of Simplot, 249 F.3d 1191, 1195 (9th Cir. 2001)

A Primer on Buy-Sell Agreements

A buy-sell agreement defines the terms and conditions of the future sale of an interest in a business. If well-written, it can smooth the transfer of an ownership interest under disruptive circumstances. If not, it can result in sharp disagreement. Unfortunately, I regularly encounter business owners with poorly written or nonexistent agreements. This article is a primer on the use of buy-sell agreements and important things to consider when writing them.

Transfer clauses in buy-sell agreements may be triggered for many reasons including:

- death or disability

- retirement

- termination of employment

- divorce

- bankruptcy

- receipt of a third party offer

Having an agreement in place that outlines the wishes of the owners may give an owner a ready market for his or her business interest, resolve estate liquidity issues, provide a framework for establishing the purchase price of an ownership interest, or reduce shareholder disputes. A typical well-written buy-sell agreement will specify details such as:

- the standard of value and value methods to be applied

- triggers that cause a buyout

- an appropriate valuation date

- payment terms

- funding methods

- non-compete agreement terms

- permitted interest transfers

Standard of Value

It is critical that business owners agree on the standard of value to be applied upon a triggering event. A common standard of value for buy-sell purposes is fair market value. Under a fair market value standard, a partial interest in a company might be worth considerably less than its pro-rata value because of potentially applicable adjustment to value such as those for lack of control or lack of ready marketability. It is important to understand and plan for the effect on share value that these adjustments may have under each type of triggering event.

Fair value is another standard of value. Fair value is typically defined by statute and case law in the state in which a company is organized, and commonly is interpreted as that which is fair or equitable. In some states, the definition includes consideration of discounts for lack of control or marketability and in others, it does not. It is important that business owners agree upon a definition of this standard if it is going to be used for buy-sell purposes. In states in which it is not subject to discounts, fair value is typically a pro- rata value of 100% of the equity in a company. Broadly, 10% of a company worth $100 would be $10 under those fair value statutes. The exclusion of valuation discounts may be appropriate under certain triggering events.

Value Methods

- Independent assessment of value - This determination of value typically utilizes one or more valuation analysts to opine on the value of a business interest. If it is agreed that an independent assessment is to be the method in which the value of a business interest is determined, the parties must decide how to select the professional(s), how many to use, and how to reconcile differences in valuation opinions if multiple appraisers are utilized. Overall, it is important to select (an) experienced, credentialed professional(s) to determine value.

- Formula pricing - This method does not equal fair market value but is rather, a means to estimate a value in an ownership interest. Formulas appeal to many parties to buy-sell agreements because they are objective and inexpensive to determine. They may, however, miss subjective factors that influence fair market value. Clients using a formulaic price should revisit it periodically to make sure the resulting value is still representative of their intentions. A formula can become outdated very quickly and its use for buy-sell purposes is generally not recommended.

- Book value - Value is sometimes defined as net book value as recorded in the entity's records, tax returns, or as determined under generally accepted accounting principles (GAAP). This value may be based on a company's financial statements, an independent audit, or tax return information. Net book value is typically indicative of historical cost and not fair market value at all.

- Value based on insurance proceeds - In a buy-sell agreement, it is not uncommon for the purchase price of an interest in a closely-held company to be the amount of an owner's life or disability insurance policy proceeds. While this is a simple method, it may or may not approximate fair market value. This potential variance may cause problems for the redeemed owner. Its use for buy-sell purposes is generally not recommended.

- Periodic review and consensus -A company with several owners may periodically hold meetings to review and update an agreed upon value. Buy-sell contracts with a static value provision will need to be modified at regular intervals. Owners must resolve how often the contract should be updated, how those changes will be documented, and what happens if the agreement is not updated. Owners should ensure that all changes to the agreement are documented and properly executed. In practice, it is more often the case than not that the adjusting process is neglected and the agreed value is outdated.

The Agreement Process

To draft a buy-sell agreement that satisfies all owners and helps preclude future conflict, owners need to understand their goals, their options and how specific facts may affect a future transaction. Discussion points that parties to a buy-sell agreement must resolve may include:

- Selecting the standard and definition of value the agreement will use

- Deciding whether to employ an independent business valuator

- Making sure the agreement clearly defines the procedures that are to be applied to determine purchase price

- Making sure the agreement anticipates the funding requirements of a buyout and defines the payment terms

- Including a provision in the agreement that requires the purchase price on the death of an owner to be no less than the value of the shares "as finally determined for federal estate tax purposes"

- Making sure the valuation provisions don't provide an incentive for new shareholders to cause a triggering event and be bought out

- Including a penalty for leaving early/misconduct/involuntary misconduct

- Considering a shareholder's divorce - Many entities want to protect the business against an owner's spouse obtaining an interest. If so, include language in the agreement to require the purchase of a spouse's ownership interest should he/she end up with stock in a divorce settlement. In any event, it is common to require a business owner's spouse to become a party to the agreement. Spouses should obtain independent legal counsel. Note: If a purchase provision is invoked, the divorcing owner's interest in the business may be diluted.

- Requiring new stakeholders to be a party to existing buy-sell agreements before becoming shareholders - Make sure the valuation provisions don't provide an incentive for stakeholders to cause a triggering event and be bought out.

Buy-sell agreements can be a valuable tool for closely held business owners who want to protect their ownership interests. But if drafted improperly, these contracts can lead to problems for both buying and selling parties. Including language that accounts for the above factors can go a long way toward the successful transfer of a business interest.

Once again another year is speeding by. I hope you and your family have a great Thanksgiving holiday. Oh and, Go Cowboys!

GRWAppraisalServices.com*512.574.3444*GRWAppraisal@gmail.com