We offer this newsletter to provide insight into current information and trends in business and the appraisal industry. We hope you find it enriching and welcome any questions or comments you may have.

For more information about our practice please visit our website at GRWAppraisalServices.com or call us at 5125743444. Enjoy!

Why some bank economists think the Fed won't raise rates until December

Talk of the Federal Reserve raising the federal funds lending rate has occurred for some time now and taking action has been put on hold for just as long. Following is an article from the Austin Business Journal regarding the Fed's rate policy.

Primarily, as it is well known the Central Texas economy has lead the country in its general immunity to and recovery from the Great Recession. As Federal Reserve rate decisions are in effect made on a national level, strong local economies and businesses may benefit from the Fed's conservative action or inaction. The federal funds rate is a driver for the prime lending rate, a rate that is the benchmark for most business loans.

Bank economists and Federal Reserve governors have a lot in common: They're more cautious about their expectations for the economy after a lousy first quarter, but they still expect growth to pick up in the second half of the year.

That's why the American Bankers Association's economic advisory committee thinks the Fed won't start raising interest rates until at least September, and four of the panel's 15 bank economists think the Fed will wait until December. None of them think the Fed will start raising its federal funds rate at this month's meeting.

The chances of a June rate hike have "basically vanished," said committee chair Ethan Harris, cohead of global economics research at Bank of America Merrill Lynch, at a news conference at the association's headquarters in Washington, D.C. "The Fed is ready to move once the data show clearly that the weak first quarter was an aberration," Harris said. So if consistently good economic data start to roll in, chances are good for a September rate hike. "They don't need to be screamingly positive numbers," Harris said.

Once the Fed starts raising rates, they will do so gradually, bank economists expect. A year from now, the federal funds will only be in the 1 percent to 1.25 percent range, they predict. That's higher than the zero to nearzero rates the Fed has maintained since the peak of the financial crisis, but it's still low. Harris thinks the Fed signaled was ready to stop juicing the economy once it announced its decision on interest rates would be data dependent. The problem is "this has been a wild period for the economy," he said.

Under traditional economic models, "We should have a boom in consumption now." Business investment also should pick up in the coming months, he expects. Past lulls in capital expenditures occurred when there was a major crisis that hurt corporate confidence, such as the debt ceiling showdown or a government shutdown. It takes more to scare businesses now, however, since all of those crises eventually resolved. "We've seen it all before," Harris said.

Conservative and telegraphed policies of the Federal Reserve help raise business owner confidence and willingness to invest. With strong local conditions, access to affordable capital continues to provide economic momentum. It appears business owners can expect continued support from Fed policies for the foreseeable future.

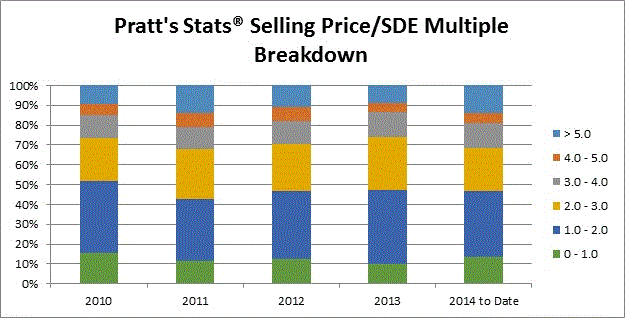

Selling price/SDE multiples

Business Valuation Resources shares its most recent research on the Pratt's Stats distribution of selling price to seller's discretionary earnings (SDE) multiples. Pratt's Stats, a database of transactions of privatelyheld companies, is widelyused by the business appraisal profession for company pricing information. SDE is defined in the database as operating profit + owner's compensation + noncash charges.

The data in the graph below include only private buyer transactions with a sellingpriceto SDE multiple from 2010 to the present. The data were separated by year and then sorted by a sellingpricetoSDE multiple. The general trend is that the majority of transactions have a sellingpricetoSDE multiple between 1.0 to 3.0. Note that the multiple range breakdown is generally consistent from yeartoyear for the years presented.

Note: Data are based on private buyer types. Source: Pratt's Stats, available at www.BVMarketData.com. Created on Sept. 4, 2014.

The use of transaction data to determine appropriate valuation multiples is utilized in the Market Approach and is one of the three general valuation methodologies used by appraisers.

Personal Goodwill vs. NonCompete in Divorce

In a ruling provided in Mauceri v. Mauceri, 199th District Court, Collin County, Texas, No. 199505372013 the court weighs personal goodwill, noncompete agreements, and equity in a recent divorce case decision. At issue was an insurance agency that the husband bought during the marriage. Both spouses had the experience necessary to run the business and under Texas law it was community property. The parties stipulated that the agency was worth $292,000 with a noncompete agreement and $141,000 without it.

Windfall: At trial, the husband argued that he should receive the business, but that it should be valued at only $141,000 for purposes of property distribution. The rationale he and his expert offered was that anything above that value was "personal goodwill." The wife's expert reminded the court of the parties' stipulated value, which turned on a covenant not to compete. As wife's expert explained, since the agency was valued under the fair market value standard of value, nonsaleable personal goodwill was by definition excluded from the value. Moreover, since the business was not going to be sold to a third party but rather would go to the husband, the undiscounted, higher value was applicable. Awarding the husband the business while applying a discount for the lack of a noncompete would be a windfall. The court discredited the husband's claim that he could just go across the street and open another agency. He would be competing against himself, which defied logic, the court found.

On the stand, wife's expert used a hypothetical to further clarify the issue. Assume the husband and wife paid cash for a business that was worth $1 million with a noncompete and $300,000 without the agreement. Two years later, after the noncompete has expired, the husband files for divorce. If the business is performing exactly as it was at the time of the purchase, its worth has not changed. Yet, based on the husband's logic, one had to assume there was a difference in value and it was attributable to "personal" goodwill.

When the husband's expert was asked how $700,000 of the $1 million paid in cash would suddenly turn into "personal" goodwill, she did not know but suggested the court could disproportionately divide the remaining assets of the marital estate in order to make up for the discrepancy. The court declined to do so and adopted the $292,000 value.

Takeaway: Though the decision to include personal goodwill in a marital estate may be jurisdictionally dependent, the wife's attorney says expert testimony "really exposed to the court how inequitable the application of the personal goodwill discount would have been in this context," he says. No appeal has been filed.

Inside the mind of the IRS re: reasonable compensation

Valuation analysts can now get a rare look at how the IRS examines reasonable compensation cases. The agency recently made public an internal document, "Reasonable Compensation: Job Aid for IRS Valuation Professionals," which has information to help valuators anticipate the challenges the IRS will make to reasonable compensation estimates. The job aid is available online as a free download. The job aid, which includes a number of appendices, examines valuation approaches, compensation data sources, suggested reading material, and court cases that shape the IRS's current thinking on this matter. It also discusses taxpayer arguments for levels of compensation that may appear to be unreasonable. For example, one argument for a high level of compensation is that an individual was underpaid in prior years. The job aid provides questions the IRS agent will ask when assessing that argument and also the relevant court cases on that specific issue. Readers can also find sample information document requests (IDRs), and examples of the market and income approaches to valuation.

If the appraisal of a business requires the contemplation of reasonable compensation that may be subject to IRS scrutiny, this publication may be a valuable resource for you or your hired expert.

Valuation of Pass-Through Entities

While there are no easy answers to valuing pass-through entities, new guidance based on years of research has been made available. A new guide Taxes and Value: The Ongoing Research and Analysis Relating to the S Corporation Valuation Puzzle written by Nancy Fannon and Keith Sellers, brings together academic research with new direction on how to value S corporations. This academic exercise provides a framework to help the progression of the business valuation profession to solve the puzzle of how taxes may affect the value of an S corporation in comparison to a C corporation.

In this resource, authors Fannon and Sellers present the findings of decades of academic research on the impact of taxes on firm value and demonstrate that historical market returns impound the effects of shareholder taxes. They also suggest a new, more direct approach to pass-through entity valuation that challenges traditional notions about the differences in value between an S corporation and the publicmarket C corporation.

Background Information: C corporations are taxed at the corporate level for federal income tax purposes. C corporation shareholders are taxed on any capital gains realized by the shareholder and on any dividend income distributed from the C corporation. In contrast, shareholders of an S corporation only pay one level of federal income tax because the S corporation will pass through all of its income and its losses to the shareholders. This difference is at the heart of the divisiveness in thought and valuation theory between pass-through and C corporations.

Chapters in this guide include:

- Chapter 1. The Importance of Matching the Cost of Capital With the Income Stream

- Chapter 2. Introduction to the Concept of Implicit Taxes

- Chapter 3. An Explanation of the Implications of Shareholder Taxes on the Corporate Cost of Capital

- Chapter 4. Literature Review: Research on the Effect of Taxes Embedded in the Cost of Capital

- Chapter 5. Impact of Prior Research on PrivateCompany Valuation

- Chapter 6. Foundation for Cash FlowBased Models

- Chapter 7. Research Related to the Magnitude of Taxes Embedded in the Cost of Capital

- Chapter 8. An Alternative Approach to the Valuation of Pass-Through Entities

- Appendix A. Suggested Areas for Further Research

- Appendix B. Evolution of Pass-Through Entity Valuation

- Appendix C. Understanding the Basics of the Cost of Capital

- Appendix D. C Corporation Versus S Corporation Transaction Pricing

- Appendix E. Digests of Cases Addressing Pass-Through Entity Issues

- Appendix F. Bibliography

- Appendix G. Links to Selected Academic Research Papers

This resource compiles years of thought around the subject of pass-through entity valuation and is a solid resource for any appraisal professional.

GRWAppraisalServices.com*512.574.3444*GRWAppraisal@gmail.com